What to expect at closing, what inspections cover, and which energy programs are available to new homeowners in Southern New Brunswick.

Quick Answer

New Brunswick charges a 1% land transfer tax with no first-time buyer exemption, most homes were built before 1980, and your home inspection is the one document in the transaction prepared exclusively for you. Eligibility rules apply to work permit holders, and multiple energy efficiency rebates can offset upgrade costs after closing.

Why This Matters

Since 2010, I have completed over 2,000 home inspections across Saint John, Hampton, Rothesay, Quispamsis, Sussex, and the surrounding communities of Southern New Brunswick. Over those years, I have watched our region welcome thousands of newcomers who arrived with professional skills, real ambition, and very little context for what buying an older Canadian home actually involves. The financial surprises, the legal nuances, and the physical realities of NB housing stock are genuinely different from what most newcomers have experienced before, and the standard homebuying guides do not cover the local detail that matters here.

New Brunswick’s housing market moves fast, and the homes here are older than most newcomers expect. Standard buying guides were not written for Maritime housing stock, local closing costs, or the programs specific to this province.

This guide covers what I wish every newcomer buyer knew before their first home inspection in Southern New Brunswick.

Whether you are relocating for work, starting a new chapter, or exploring a move to Atlantic Canada, the process of buying a home in New Brunswick involves surprises that a first-time homebuyer, or someone moving from another country, will not anticipate. This guide walks you through the financial realities, legal eligibility requirements, and the specific challenges that come with purchasing older homes in this region.

Why NB Housing Stock Is Unlike Anything You May Have Seen Before

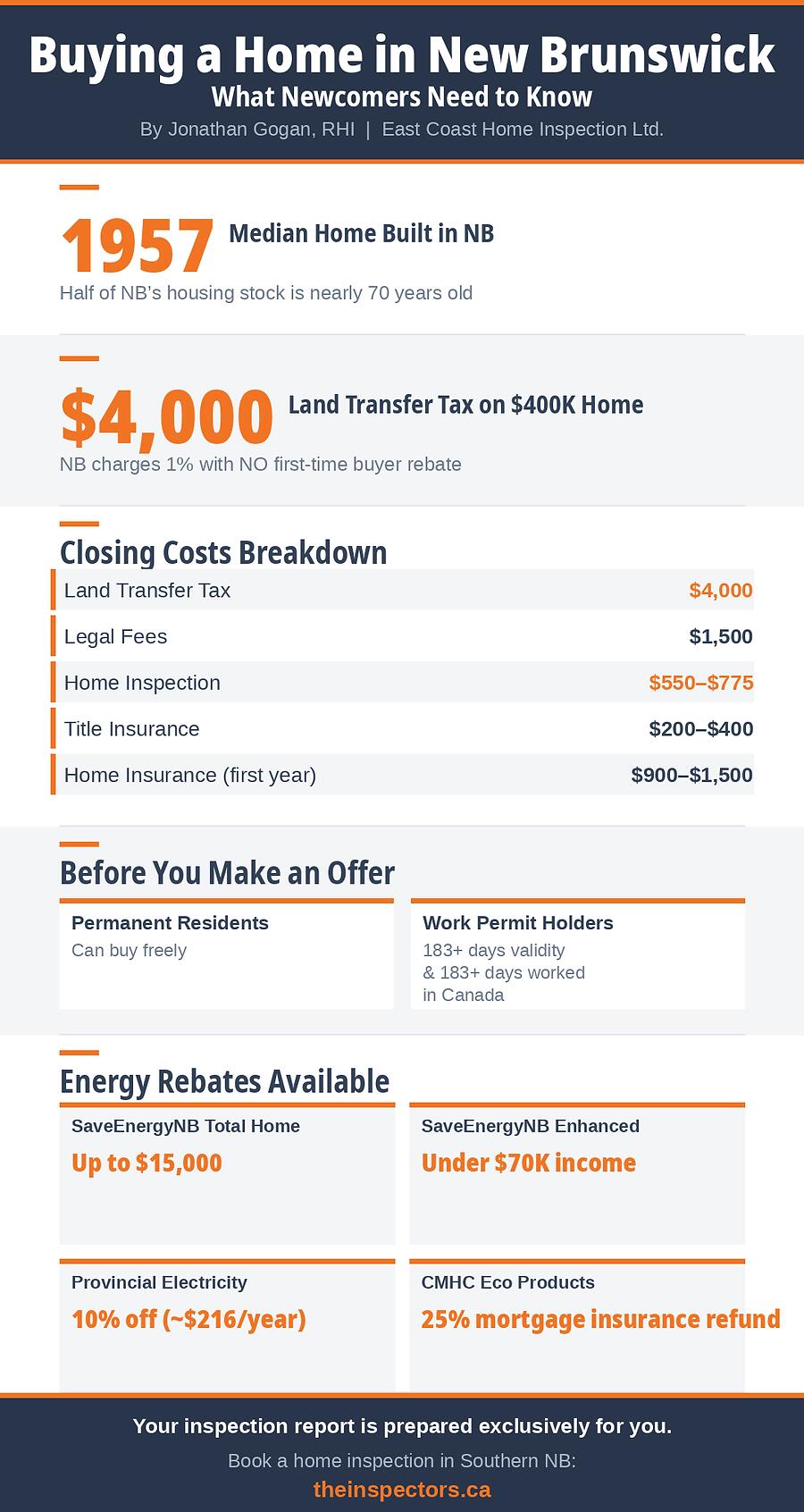

The median construction year for a home in New Brunswick is 1957. Half of the province’s housing stock is nearly 70 years old. In Saint John specifically, a significant portion of available homes dates to the 1960s and 1970s, with entire neighbourhoods that have seen minimal renovation since they were built.

This matters for two reasons. First, these homes were built with materials and systems that no longer exist in new construction: oil-fired heating, knob and tube wiring, galvanized steel plumbing, rubble stone foundations, and in some cases, asbestos insulation or lead-based paint. None of these are automatically dangerous if they are properly maintained and understood. But they require someone who knows what to look for and how to explain what they are seeing.

Second, maintaining older housing stock has become significantly more expensive. According to Statistics Canada, residential construction costs in New Brunswick rose 86.7% between 2017 and 2024. When something needs repair or replacement in an older home, the cost reflects today’s labour and material market, not what things cost a decade ago. A professional home inspection before you buy gives you a clear picture of what is there, what condition it is in, and what it will realistically cost to maintain or upgrade over time.

For newcomers moving from countries with newer housing stock, or from climates where certain systems do not exist, this context is not intuitive. It takes time to learn. A home inspector who has worked across Southern NB for over a decade can translate what you are looking at into language that helps you make a confident decision.

The Financial Surprises Nobody Warns You About

Several costs associated with buying a home in New Brunswick catch newcomers off guard, particularly those who have researched the process based on other provinces.

Based on a $400,000 purchase, budget for 2 to 3 percent of the purchase price at closing, not including CMHC mortgage insurance or moving costs. That is approximately $6,500 to $11,000 due at closing.

What You Will Pay at Closing

- Real Property Transfer Tax: $4,000. 1% of purchase price. No first-time buyer rebate in NB.

- Legal Fees and Disbursements: $1,300 to $2,600. Includes title search, deed registration, filing costs.

- Home Inspection: $550 to $775. Same-day report, thermal imaging, drone roof scan.

- Title Insurance: $200 to $400. One-time. Often replaces a formal land survey.

- Home Insurance (first year): $900 to $1,500. Required by lender before closing.

- Property Tax Adjustment: $200 to $1,500. Reimburse seller for prepaid taxes past your closing date.

- CMHC Mortgage Insurance: $8,330 to $13,300. Only if down payment is under 20%. Can be rolled into mortgage.

New Brunswick charges a Real Property Transfer Tax of 1% on the greater of the purchase price or the assessed value. Unlike Ontario and British Columbia, New Brunswick offers no land transfer tax rebate for first-time buyers. This is worth knowing early in your planning. On a $400,000 home, that is $4,000 due at closing that many newcomers have not budgeted for. The Financial and Consumer Services Commission of New Brunswick publishes a full homebuying guide that walks through all closing costs in detail, and reading it before you make an offer is worth your time.

Beyond these two surprises, budget for your inspection fee, legal fees and disbursements, title insurance, an appraisal, and if the property is on a private well, water testing. If your down payment is below 20%, you will also pay mortgage default insurance through CMHC. Going in with a realistic picture of total closing costs prevents the kind of last-minute financial stress that takes the joy out of what should be an exciting milestone.

Know Your Eligibility Before You Make an Offer

Canada’s Prohibition on the Purchase of Residential Property by Non-Canadians Act remains in effect until January 1, 2027. This federal legislation restricts certain non-Canadians from purchasing residential property in Canada, and the rules are specific enough that misunderstanding your status creates real legal risk.

If you are a Permanent Resident, you are exempt from this restriction and can purchase property freely. If you are in Canada on a work permit, you must meet two specific criteria before you can legally sign a purchase agreement: your work permit must have at least 183 days of validity remaining at the time of purchase, and you must have worked in Canada for a minimum of 183 days in the preceding 12 months. The Government of Canada’s official guidance covers the full eligibility rules and exceptions.

Confirm your status with a real estate lawyer before you begin actively searching for a property. Getting this wrong does not just cause delays. It can result in a transaction that needs to be reversed.

Building Canadian Credit Before You Buy

One of the most consistent barriers newcomers face when applying for a Canadian mortgage is the credit history gap. Canadian lenders typically do not recognize credit history from other countries. Regardless of how strong your financial record was at home, you arrive in Canada effectively starting from zero in the eyes of a Canadian lender.

The practical response is straightforward: begin building a Canadian credit history as early as possible after you arrive. A secured credit card or a credit-builder product from a Canadian bank, used regularly and paid in full each month, establishes the track record that lenders need to see. CMHC offers specific mortgage products for newcomers with limited Canadian credit history, including down payment options as low as 5% for Permanent Residents.

It is also worth understanding the rental context. Rent growth in New Brunswick is currently running at 6%, which is well above the general inflation rate of around 2%. For newcomers who are renting while saving for a down payment, that gap makes the timeline longer than it used to be.

What NB Winters Do to Older Homes

Southern New Brunswick has a genuine winter. Extended cold, significant snowfall, freezing rain, and freeze-thaw cycles leave evidence behind in older homes. Reading that evidence accurately is a significant part of what a home inspection in this region covers, and it is one of the areas where local experience makes the most difference.

Ice dams form when heat escapes through a poorly insulated attic, melts the snow on the roof, and refreezes at the cold edge of the eaves. The water backs up behind that ice ridge and finds its way under the shingles and into the structure. The signs are not always dramatic. Water staining on a ceiling near an exterior wall, damaged insulation in the attic corners, and peeling paint at the soffits all point toward the same underlying issue. Repairs typically run $2,000 to $5,000 depending on the scope of reroofing and attic remediation required.

Basement water is one of the most common findings in Southern NB homes. Spring is when it becomes visible. I look for evidence of past water entry even in a currently dry basement: white mineral deposits on concrete block walls (called efflorescence), rust staining at the base of steel columns, and flooring damage near the perimeter. A dry basement in March does not mean a dry basement in April. Addressing basement water typically costs $1,500 to $4,000 depending on whether the solution is interior sealing, exterior grading adjustment, or a combination of both.

Frost heave refers to what happens when soil around a foundation freezes, expands, and shifts over decades of New Brunswick winters. Doors and windows that stick, cracks running diagonally from corners, and uneven floors can all be connected to long term foundation movement. Understanding the difference between cosmetic settling and a structural concern is part of what you are paying for in an inspection. Addressing foundation settling can cost anywhere from $500 for simple cosmetic crack repair to $15,000 for underpinning in severe cases.

Heating system condition matters more in this climate than it does in a moderate one. A furnace or heat pump that has worked hard through 15 or 20 NB winters needs honest evaluation of its age, service history, and realistic remaining service life. Budget $3,500 to $6,000 for a mid-efficiency oil furnace replacement, or $6,000 to $10,000 for a heat pump installation with backup electric heating.

Rural Properties: Wells, Septic, and What Your Lender Will Not Tell You

If you are looking at properties in Hampton, Sussex, or the rural communities throughout Kings County, there is a meaningful chance the property is on a private well and septic system rather than municipal water and sewer. This is entirely normal in rural New Brunswick, and it does not make a property less desirable. It does add layers to the transaction that your lender’s standard checklist may not fully address.

A private well supplies your drinking water directly from the ground. Water quality should be tested before you finalize any purchase. The standard tests cover bacteria and nitrates, which are the primary health concerns, but depending on the property’s location and history, other contaminants may be worth testing for. During a home inspection, your inspector will evaluate the well casing, pressure tank, and associated plumbing. A separate water quality test from a certified laboratory is also recommended and sometimes required by your lender. Budget $300 to $600 for comprehensive water testing including bacteria, nitrates, and mineral analysis.

Septic systems treat and dispense household wastewater on the property. A properly maintained system can function reliably for decades. One that has been neglected, undersized for the home’s occupancy, or installed incorrectly can fail in ways that are both expensive and disruptive. During an inspection, I assess what is accessible and visible, note the approximate age and type of system, and flag anything that warrants a closer look from a licensed septic specialist. A septic system replacement can cost $4,000 to $12,000 depending on soil conditions and system size, which makes this due diligence essential before closing.

The lender’s minimum requirements around well and septic are not the same as what is in your best interest as a buyer. Ask your inspector what they recommend for the specific property, beyond what the mortgage approval process requires.

The Energy Efficiency Layer and the Rebates Available to You

Older Southern NB homes often have significant room for energy efficiency improvement. Insufficient attic insulation, original single-pane windows, aging oil furnaces operating well below peak efficiency, and unsealed basement rim joists that allow cold air to enter along the foundation are common findings. For a newcomer arriving from a warmer climate, a New Brunswick heating bill in January can be a surprise.

The good news is that meaningful financial programs are available to help. The SaveEnergyNB Total Home Energy Savings Program, delivered through NB Power, offers an average of $1,700 in rebates to homeowners who complete qualifying upgrades, with some households receiving up to $10,000 depending on the scope of work. The SaveEnergyNB Enhanced Energy Savings Program provides additional support for households with a combined gross income under $70,000, covering insulation, ventilation, and heat pump installations. The provincial government’s electricity rebate provides a 10% reduction on electricity consumption, saving the average household approximately $216 annually.

If you are using CMHC mortgage default insurance, there is an additional incentive worth knowing about. CMHC’s Eco Products line offers a 25% partial refund on your mortgage insurance premium if you purchase an energy-efficient home or commit to qualifying energy improvements after closing. This is a meaningful saving that many buyers never discover.

Your home inspection report is, among other things, an energy map of the property. What I find in the attic, the basement, and at the heating system corresponds directly to what you will spend each winter. Understanding that picture before you close helps you budget realistically and take advantage of the programs designed to help you improve it.

How to Use Your Inspection Report as a Newcomer in Southern NB

A home inspection report is not a pass or fail document. There is no score, no grade, and no verdict on whether you should buy the home. It is a written record of the condition of every major system and component of the home at the time of the inspection, delivered in plain language and supported by photographs.

Items are organized by category. Some require immediate attention. Some are flagged for monitoring. Others are simply documented for your awareness. The inspector’s role is to give you an accurate picture of what you are buying. The decision itself belongs to you.

Read the report carefully, and read it with your real estate agent. Use it as the basis for any conditions or renegotiations you want to pursue before closing. At East Coast Home Inspection Ltd, post-inspection support is included at no extra charge.

In a fast-moving market, buyers sometimes face pressure to waive the inspection condition to make an offer more competitive. My experience across more than 2,000 inspections in this region is consistent: the purchases that cost buyers the most in unexpected repairs after closing are almost always the ones where no inspection was done before the sale.

For newcomers navigating an unfamiliar market, an unfamiliar housing stock, and a process that may look quite different from homebuying in your country of origin, the inspection is the one moment in the transaction where someone is working entirely on your behalf.

Frequently Asked Questions From Newcomers to New Brunswick

Do newcomers to Canada need a home inspection in New Brunswick?

Yes. A home inspection is not legally required in New Brunswick, but it is strongly recommended for any buyer unfamiliar with older Canadian housing stock. Most homes in Southern NB predate modern insulation and electrical standards. An inspection gives you a written condition report before you commit to the purchase.

Is there a first-time home buyer land transfer tax rebate in New Brunswick?

No. New Brunswick eliminated the first-time buyer rebate on the Real Property Transfer Tax. Every buyer pays 1 percent of the purchase price at closing regardless of purchase history. This is different from Ontario and British Columbia, where rebates still apply for qualifying first-time buyers.

How long does a home inspection take in Saint John or Southern NB?

Most inspections in Southern New Brunswick take two and a half to three and a half hours depending on the size and age of the home. Older homes with oil heating systems, older electrical panels, or finished basements typically take longer. You receive the full written report the same day.

What are the closing costs for buying a home in New Brunswick?

Budget 2 to 3 percent of the purchase price in closing costs, excluding CMHC mortgage insurance and moving expenses. On a $400,000 home that is roughly $8,000 to $12,000. The largest single cost is the Real Property Transfer Tax at 1 percent of the purchase price, with no first-time buyer rebate in New Brunswick.

What energy rebates are available to new homeowners in New Brunswick in 2026?

SaveEnergyNB offers up to $15,000 in advance funding for heat pump and insulation upgrades through the Total Home Energy Savings Program. Households with combined gross income under $70,000 may qualify for free upgrades through the Enhanced program. A Home Energy Evaluation is required to access both.

Can I attend my home inspection as a buyer?

Yes, and you should. Walking through the home with your inspector gives you direct context that no written report can fully replace. It is especially valuable for newcomers unfamiliar with Canadian home construction, heating systems, or older building standards common in Southern New Brunswick.